Differential Cap Rate Analysis

Differential Cap Rate Analysis

How are increasing interest rates and inflation affecting cap rates? A quick calculation.

Buyers and sellers of commercial real estate investment property are all asking the same question about increasing interest rates and inflation: How do increased borrowing rates and inflation affect the value of real property?

What they are really asking is several questions:

How does the increased cost of capital affect the asking/selling price of property, and the application of a cap rate to the NOI?

Does the increased cost of capital increase the risk of default on tenant leases, particularly for tenants who had to borrow to survive the pandemic, or have to borrow now to pay for inflated inventory and operating expenses?

How does that added risk of tenant default affect the cap rate on an income property where the buyer demands a higher return for assuming a perceived higher risk?

How can we calculate/quantify the impact on cap rates in an environment of increasing interest rates and increasing risk?

These are complicated questions and because every property is unique, every property has a different risk profile, and every buyer/seller has a different methodology for calculating risk/return, I offer up a “back of the envelope” method for calculating the change in cap rate based on a change in interest rate.

I call this “back of the envelope” method a “Differential Cap Rate Analysis.”

To calculate the Differential Cap Rate, a few variables are necessary: 1) current interest rate; 2) expected change in interest rate; 3) amortization period; and, 4) buyer’s expectation of return on its invested capital (cash). We also need to know the LTV and how it “might” change with a change in interest rates.

Also, a basic understanding of a mortgage constant is necessary. A mortgage constant calculates the monthly payment of interest and principal on an amortizing loan. The mortgage constant is calculated by Excel using the =PMT() function.

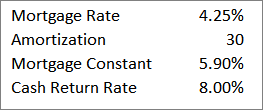

As a starting point, I assume the following (but the analysis is the same regardless of your starting assumptions): Finance Rate: 4.25%, 30-Year Amortization, LTV 75%, and Return on Invested Capital of 8%. From the interest rate and amortization period, Excel calculates the mortgage constant at 5.90. The investor requires a return on its invested capital of 8%.

With a 75% LTV, we then take a weighted average as follows: 75% of the cap rate will be based on the mortgage constant (5.9%); 25% will be based on the Return on Cash (8%). As shown below, 75% of 5.9% equals 4.427%. 25% of 8% equals 2%. Add the two together for a base cap rate of 6.427%.

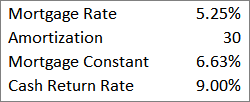

Now, let’s look at changes. Increase the interest rate by 1% to 5.25% and the mortgage constant recalculates to 6.63%. Leave the amortization period alone (but you could change it). Change the desired return on cash invested to 9% to reflect increased risk to the buyer.

And, apply the same weighted average to the new mortgage constant and desired rate of return. The new or differential cap rate based on these changes is now 7.22%, or .793% higher.

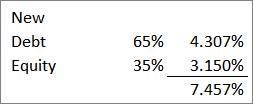

Changing the Debt/Equity Ratio to 65/35 also changes the differential cap rate. With tightening credit, LTV may become more restrictive.

The spreadsheet does the calculation for you. As you can see, if the buyer has to put in more capital (cash), the cap rate increases. This makes sense because the buyer requires a higher return on his capital than the cost of borrowing, that difference is reflected in a higher cap rate (lower purchase price) to accommodate the desired return on the investment.

Please remember that this is just a “back of the envelope” calculation. For an explanation of the =PMT() function, click here. For a deeper dive into the weighted average approach to cap rate calculation, click here. For a copy of the spreadsheet (Substack doesn’t accommodate embedding), send me an email.